The economic outlook for Rhode Island has improved considerably over the last three years. This is particularly evident given a significant decline in the unemployment rate, which was 5.4 percent in February 2016 compared with a peak rate of 11.3 percent in August 2010. In addition, during the last three years all major industries have added jobs in Rhode Island. The improvements in the economy, however, are not good enough to overshadow troubling signs of major long-term structural problems in the state.

As of February 2016, the state had recovered only 82 percent of the jobs lost during the Great Recession. In addition, economic growth has been persistently slow in Rhode Island. It is not all about the recession, however. The state’s problems started a long time ago. It seems that the early 1990s marked the reversal of the fortune for Rhode Island. It has been unable to build a competitive economic base that can take advantage of opportunities generated by the post-industrial economy.

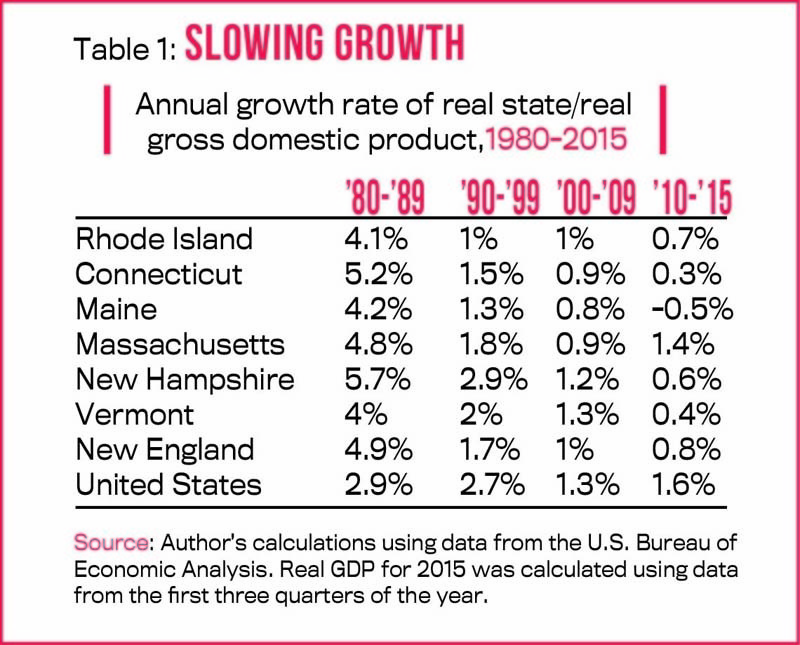

Rhode Island had a vibrant and fast-growing economy and ranked among the top 10 fastest personal income-growing states in the 1980s. But there was a fundamental shift in the state’s economic performance in the early 1990s. Between 1990 and 2009, Rhode Island ranked among the worst-performing states in the nat ion in terms of job creation and overall economic growth. The growth rate of the gross state product declined from an annual average of 4.1 percent from 1980 to 1989 to 1 percent between 1990 and 2009. From 2010 to 2015 it was 0.7 percent.

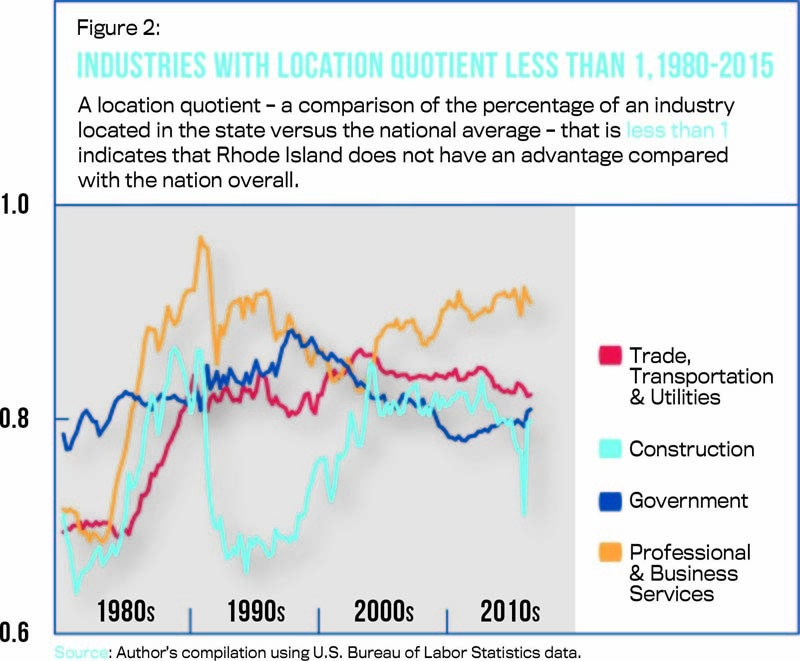

And the slowdown was broad-based, affecting all industries in the state, as demonstrated by the Location Quotient in Figures 1 and 2. The location quotient is calculated as the ratio between the state’s share of employment of a specific industry divided by the national share for the same industry. A high LQ (well above 1) implies competitive advantage in that industry. A decline in the LQ indicates loss of competitiveness, while an increase in the LQ indicates that a specific industry is growing relatively faster in the state compared to the nation.

Figure 1 shows that Rhode Island has comparative advantage (LQs greater than one) in education and health services, manufacturing, finance, and leisure and hospitality. However, the long-term trends are worrisome because they indicate a stark decline of the state’s competitiveness in manufacturing, and in education and health services, which are core industries that have large multiplier effects on other sectors of the economy, create high-paying jobs and are pillars of long-term economic growth. Together these industries account for about 30 percent of all jobs based in the state.

So while Rhode Island added jobs in education and health services over the last three decades, a declining LQ implies that the education and health services sector in the state is not growing as fast in the national economy. In addition, manufacturing lost about two-thirds of its employment base during the last 3 decades, causing the manufacturing location quotient to decline from about 1.5 in the early 1980s to 1 in 2015. This indicates a major loss of manufacturing competitiveness in the state.

On the bright side, the state has improved in both the finance, and leisure and hospitality sectors. The competitive gains in finance, however, are mostly due to the re-location of operations of Fidelity Investments to Smithfield in the late 1990s.

The location quotient for trade, transportation, and utilities, professional and business services, and construction are all less than 1 (see Figure 2). This indicates that these industries performed poorly in the long term in Rhode Island. It is worth noting that there were significant gains in competitiveness in trade, transportation, and utilities and in professional and business services in the 1980s in Rhode Island, but these industries have barely managed to maintain their competitive position during the last two decades.

The location quotient for the government sector has been hovering around 0.8 since the early 1980s. This suggests that the size of the government in Rhode Island is relatively small compared to the national average and has not changed significantly since the 1980s.

The discussion above suggests that Rhode Island missed the growth-train because its economy is no longer aligned to compete in a globalized economy. The widespread factual perception that Rhode Island is a costly and unfriendly place in terms of regulations has sent away businesses and people who would contribute to create jobs and income in the state. This has to change.

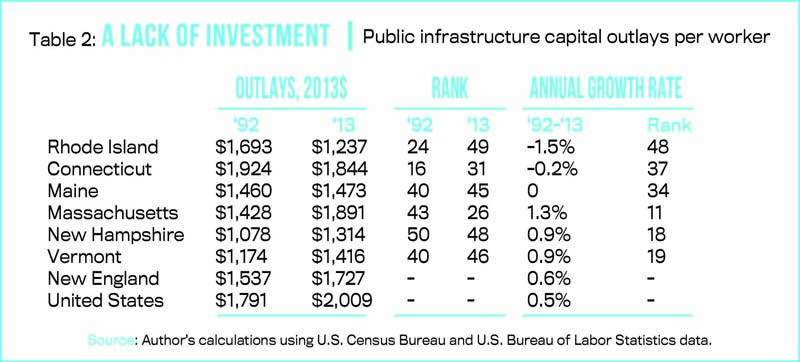

In addition, the state cannot afford to be ranked 49th in terms of public capital investment in infrastructure (see Table 2). Policymakers must find ways to increase public capital investments in strategic areas if they want to increase competitiveness and support business development in Rhode Island.

Rhode Island’s economy will thrive if the state turns into a friendly place for businesses and people, increases public investments on infrastructure, prepares its workforce for the Knowledge Economy and takes advantage of its competitive advantages. •

Edinaldo Tebaldi is an associate professor of economics at Bryant University.